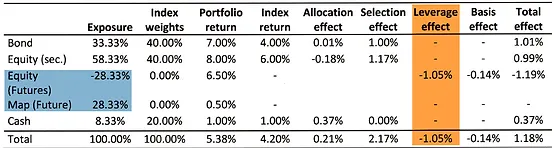

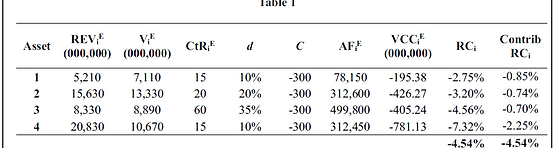

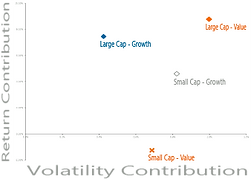

In this article, we propose a methodology to measure the effective contribution to the total risk and to the tracking error due to asset allocation or selection.

In this article, our CEO, Philippe Vandooren, explains how we support our clients in managing their portfolios and solving their ever-evolving challenges

Philippe Vandooren (CEO, AMINDIS) was on BFM TV to present his vision for successful software development projects

Video

Fichier vidéo

Date

18.10.2022

How to measure the Transition Risk of your Portfolio

This method aligns with the New I.R.R (Impact, Risk, Return) approach

Video

Date

18.03.2021

Webinar Finance durable Integration

The Future of Sustainable Finances From regulatory agenda to product integration

Video

Date

18.10.2022

AMINDIS NEW B.I.R.R

A unique solution allowing you to solve the Impact, Risk, Return equation with a holistic view across all business functions for premium investment decisions!

Video

Date

15.02.2020

Empower your external clients experience

Empowering external clients on their private cloud.

Video

Date

02.01.2020

How to empower your external clients experience?

Empowering external clients on their private cloud

CSRD & ESG: AMINDIS hosts strategic webinar on May 22

Body

CSRD is here — are you ready? Join our webinar on May 22 to discover how to simplify ESG reporting, assess materiality, and ensure compliance with confidence.

Shape the future of Finance at the ALFI Global Asset Management

Body

AMINDIS invites you to join the ALFI Global Asset Management - Conference on March 19 and 20, 2024, hosted at the European Convention Center in Luxembourg.